CALL US TODAY: 775 415 - KIRK (5475)

Register for Our Next Live Webinar:

"The Momentum-Maker Mastermind: Mindset, Methods, & Metrics"

Join Kirk on April 12th @9:45 AM (Pacific Time)

GET FUNDED FAST FOR HOME AND BUSINESS!

Kirk Jaffe Enterprises, Inc. has funded thousands of companies just like yours. Contact Us today to Get Started!

Our Services

Kirk Jaffe Enterprises, Inc. has multiple services for home buyers and business owners.

Make us your preferred solution for home and commercial real estate.

MORTGAGE LENDING

We offer the most competitive rates and excellent service beyond closing. Guaranteed! PRO.

REAL ESTATE AND PROFESSIONAL CONSULTING

We offer guidance to real estate professionals, tax professionals, lawyers, and CPA's.

BUSINESS CONSULTING

Are you ready to grow your business to

the next level and beyond. Kirk has helped hundreds of businesses and

can help you get there faster.

INVESTMENT ASSISTANCE

Our proven track record in solid investments has help hundreds and could help you too. Ask us how!

FIND OUT WHY KIRK JAFFE IS THE BEST CHOICE FOR LOANS AND HELPING BUSINESSES GROW!

Kirk Jaffe, CEO/Founder – Executive Management of $200MM private investment fund including Mortgage Notes, Real Estate Owned (REO) and Commercial Property Holdings. He has overseen and held executive authority of over 20,000 real estate transactions in his 20-year real estate career including buying and selling of property, foreclosure, short sale, loan modification, rehabilitation of property with an aggregate over $1 Billion value. Kirk has also originated over $ 1 Billion of new Mortgages.

Kirk is the past President of the Universal City/North Hollywood Chamber of Commerce as well as a former co-chair of the ALFN Commercial Practices Committee. He is active as a speaker and moderator of several trade organizations including the CA Mortgage Bankers Association (CMBA), Mortgage Banking Association (MBA), and the Attorney Legal Financial Network (ALFN). Mr. Jaffe is quoted or has been a guest of several media outlets including: KABC790 Talk Radio, NBC and the Los Angeles Daily News to name a few.

Kirk Has Appeared On:

How Can We Help

You Today?

Start Quote

Change Plan

Contact

Let Us Know What You Need!

We custom fit every service to your personal business needs. Whatever it is, we have a solution. Just click the button below to get assistance today!

If you're looking for a firm who can help you with not just your mortgage, but help you GROW YOUR BUSINESS FAST... you're where you should be!

MORTGAGE LENDING

We offer Custom Tailored mortgages for Home or Business!

BUSINESS CONSULTING

Grow your business FAST with our Business Consulting Services!

INVESTMENT CONSULTING - REAL ESTATE ASSETS

Our win/win approach to investing has helped hundreds. FIND OUT MORE!

REAL ESTATE PROFESSIONALS

If you are a real estate professional and are ready to work with a partner with years of experience, you're in the right place.

CPAS, ATTORNEYS, AND INSURANCE PROFESSIONALS

If you have questions about the potential legal implications of real estate transactions for your clients, Kirk Jaffe has the answers!

GET STARTED TODAY

Getting started with Kirk Jaffe Enterprises is super easy. Find out how it works below!

WHAT OUR CLIENTS HAVE TO SAY

“What a GREAT guy Kirk is! I highly recommend him and his services all the time and for my own home loan needs. Why would I say that as a Broker myself? Well as a Buyer and a Broker I cannot have my hand into many aspects of the transaction, so I trust Kirk with my financing needs he has yet to let me down! "

Steve Duncan

"Kirk is my go-to lender. He has worked many “miracle situations” and provides top notch service from start to finish...."

Jeff J. Grice

"I have known Kirk Jaffe for many years. Kirk has a stellar reputation. You can see his reviews by going to www.mycity.com/profile/kirk-jaffe."

Bob Friedenthal

"When I need any information regarding the Real Estate Financing space for a client, my first call is to Kirk Jaffe. He is knowledgeable, professional, and experienced. He stays on top of cases and follows up with clients. He is a true asset to my business."

Bruce Fine

"Kirk works hard and well day and night, a kind person and gets it done fast!"

Melissa Oppenheimer

"Kirk did a fabulous job. He walked me thru the process and it was incredibly easy compared to other mortgages I've done. Thanks to Kirk, my house closed in under 21 days, and he got me a great interest rate."

CHARLIE JEWETT

WHY WORK WITH KIRK JAFFE ENTERPRISES, INC?

Because we offer the best service at affordable rates and will help your company grow faster! Click the button or

CALL US AT (775) 415 - KIRK (5475)

Freddie Mac Adds New Underwriting Standards to Combat Fraud

Freddie Mac Adds New Underwriting Standards to Combat In its most substantive rule update since implementing new measures last November to remove brokers from the due diligence chain in loan documenta... ...more

Investments ,Mortgage News

April 17, 2024•2 min read

Banks’ Exposure to CRE Loans by Bank Size

When CRE hits investors, fine, they were paid to take those risks. But we’re a little more squeamish when it comes to banks. Commercial Real Estate loans amount to about $5 trillion. Not all CRE sect... ...more

Business ,Investments &Mortgage News

April 17, 2024•4 min read

U.S. Money Supply Is Doing Something No One Has Witnessed Since the Great Depression, and It Foreshadows a Big Move to Come in Stocks

M2 money supply hasn't made a move this pronounced since the early 1930s. When examined over long stretches, the stock market can't be beat. While other asset classes have produced solid nominal gain... ...more

Business ,Mortgage News

April 08, 2024•7 min read

Fed members' updated interest rate outlooks rock markets

Federal Reserve Chairman Jerome Powell wants to cut interest rates this year. He's been saying it regularly all year. But remarks from Fed officials Thursday suggested the when of rate cuts may not ... ...more

Business ,Mortgage News

April 06, 2024•3 min read

Justice Department Says It Will Reopen Inquiry Into Realtor Trade Group

The Justice Department will reopen an antitrust investigation into the National Association of Realtors, an influential trade group that has held sway over the residential real estate industry for dec... ...more

Mortgage News

April 06, 2024•5 min read

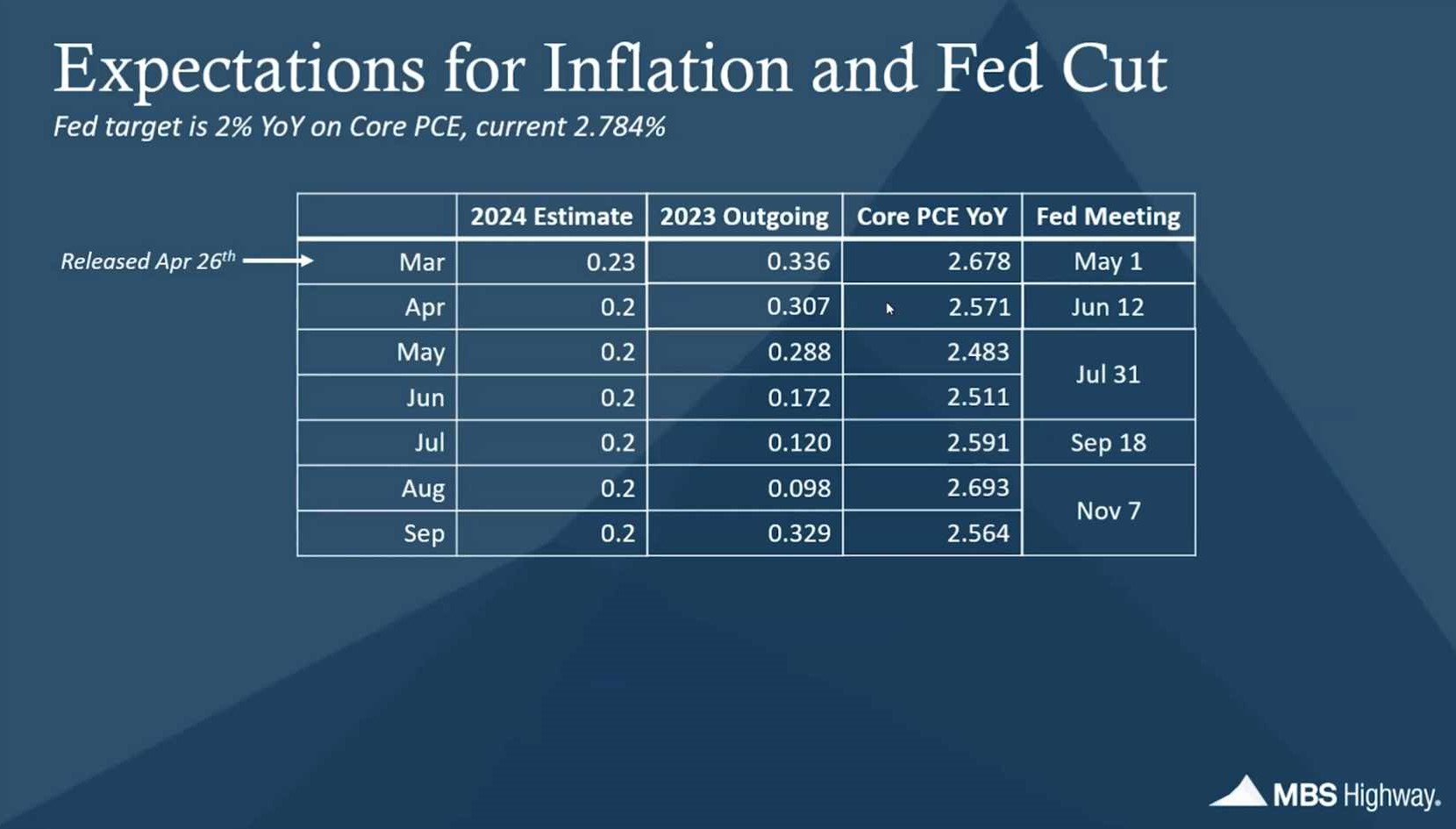

The Hidden Trigger for Federal Rate Adjustments and Its Impact on Home Buying

If you are watching the headline news and wondering when the Fed will lower rates, Tall Pinze Advisory (a sister company to KJE Inc) has the update. The two charts here show that US Consumer Spending... ...more

Mortgage News

March 29, 2024•1 min read

Connect With US

CONTACT US TODAY

Need to reach us? Send us an email or give us a call today.

Kirk Jaffe Enterprises, Inc.

195 Highway 50, Ste 104-476

Stateline, NV 89449